Why the 1% Ocean Stat Backfires With Private Capital

It signals urgency to philanthropy but risk to lenders and investors.

Less than 1% of climate finance goes to the ocean. It’s one of the most repeated stats in ocean circles, showing up in panel discussions, pitch decks, and conference keynotes. It’s accurate, but it’s also the wrong pitch for half the room.

The United Nations states that all sources combined, including public, philanthropic, and private, deliver less than 1% of global climate and biodiversity finance to the ocean, which is $3 billion against an estimated need of $175 billion a year.

For a foundation or a government donor, that number is the whole argument. It signals urgency, and urgency is what philanthropic capital responds to.

A venture investor or a debt underwriter hears something different. For them, “underfunded” reads as “unproven.” A sector that’s pulled in less than 1% of a massive global pool, after years of attention, looks like a sector smarter money already passed on. Private capital rarely wants to go first, and a scarcity stat with no context gives it a reason to keep waiting.

I spent years in marketing and communications across private credit, index funds, and venture capital, so this reaction doesn’t surprise me. It’s the same instinct behind a lender wanting three years of cash flow before discussing terms. A large part of the job is being cautious.

The part the 1% framing leaves out is that it’s a snapshot of capital raised to date, and says nothing about where that capital is headed next. Trajectory is what allocators price.

Start with how load-bearing the ocean already is. Around 80% of world trade moves by sea. Nearly 99% of international internet traffic runs through undersea cables, the infrastructure carrying every bank transfer and video call between continents.

Plus, seafood supplies roughly 20% of animal protein intake for more than 3 billion people. By the Organisation for Economic Co-operation and Development's accounting, the ocean economy was worth $2.6 trillion in 2020, large enough that if it were a country, it would rank as the fifth largest economy on the planet.

Much of the infrastructure running that economy is clunky, outdated, and unsustainable, which is where the opportunity sits.

A few fund managers are already positioning for it. Ocean 14 Capital closed its fund at €201 million for aquaculture and fisheries tech. A new $75 million Asia Ocean Fund, co-managed by Katapult Ocean, launched last fall to close the early-stage gap across the region. Aqua-Spark recently closed the first $48 million of an Africa-focused aquaculture fund. Propeller Ventures closed its debut fund above $118 million. Redstone Nordics opened a fund this year aimed at Baltic shipping, subsea cables, and offshore renewables.

These are early signals. Most funds are too new to have a meaningful track record of returning capital, even if annual reports point to real traction. Plus a track record of distributions does more for a category than one deploying capital, so the next wave of allocators will be watching exits more than fund announcements.

Capital also doesn't always need an ocean story to find its way into the industry. It can follow demands that already exist, and a growing share of that demand happens to run through ocean infrastructure.

For example, subsea cables are getting funded by AI infrastructure’s hunger for more bandwidth, and offshore wind is funded by grids that need more power. Neither investment thesis was written with the ocean in mind, but the ocean increasingly sits in the path of the capital anyway.

Policy adds another layer. A carbon removal certification framework, a fishing subsidy reform, or a subsea cable security mandate creates demand across an entire category at once. That kind of structural shift tends to move allocators faster than any individual pitch deck.

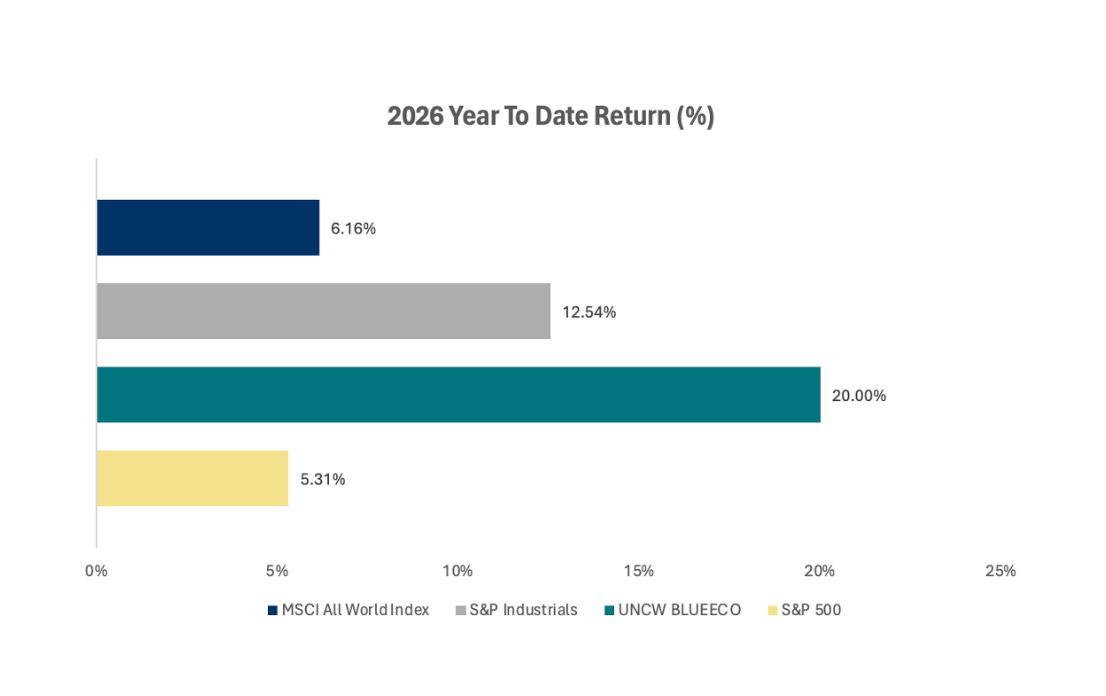

On the public markets side, the UNCW Blue Economy Index has outperformed the S&P 500 over the past year. It's a short window and worth watching rather than treating as settled, but it's another data point in the same direction as the fund closes.

None of this erases the 1% stat. It's still true, and it does real work in a philanthropic pitch. But aimed at private capital, it tells only half the story.

The fund closes, the infrastructure demand, and the early public market signals tell the other half, the part about where it's headed.

This article is part of a new spotlight series on Blue Tide, which tells a deeper story about the people, solutions and topics shaping the ocean economy. If you know someone who would like to be featured then send me an email.